High Yield Savings Account Rates Drop: 4 Critical Banking Moves Before September Ends

Are you earning just 0.39% on your savings while missing out on rates above 4.30% APY? With Federal Reserve rate cuts expected and banks already slashing returns, savvy investors are scrambling to lock in today's high yield savings account rates before they disappear. This comprehensive guide reveals the exact strategies banking experts recommend for maximizing your returns in September 2025, plus critical moves you must make before month-end to protect your financial future.

Breaking: High Yield Savings Account Rates Face Imminent Decline

🚨 Rate Alert: The CME Group's FedWatch Tool shows a 90% probability of Federal Reserve rate cuts in September 2025, potentially triggering immediate drops in savings and CD rates across all major banks.

The banking landscape is experiencing a dramatic shift as we enter September 2025. While the average traditional savings account languishes at a mere 0.39% APY according to FDIC data, high yield savings account options from top-tier banks like EverBank and BrioDirect still offer competitive 4.30% APY rates.

However, this window of opportunity is rapidly closing. Banking experts warn that mortgage refinancing rates and savings yields will likely follow the Fed's anticipated rate cuts, potentially dropping by 25-50 basis points before year-end.

| Account Type | Current Rate | Projected Rate (Dec 2025) | Rate Change |

|---|---|---|---|

| High Yield Savings | 4.30% APY | 3.80-4.05% APY | -0.25 to -0.50% |

| Traditional Savings | 0.39% APY | 0.15-0.25% APY | -0.14 to -0.24% |

| 1-Year CD | 4.50% APY | 4.00-4.25% APY | -0.25 to -0.50% |

| 30-Year Mortgage | 6.41% | 6.15-6.30% | -0.11 to -0.26% |

Why September 2025 Is Your Last Chance

- Federal Reserve meeting scheduled for mid-September with 90% rate cut probability

- Banks typically adjust deposit rates within 24-48 hours of Fed announcements

- Historical data shows 6-month lag time for rates to stabilize at lower levels

- Current rates represent 15-year highs that may not return until next economic cycle

Certificate of Deposit Rates: Lock-In Strategy Before Fed Cuts

:max_bytes(150000):strip_icc()/BestHigh-YieldSavingAccounts-cf61d112a9254710acfed7122a31a417.jpg)

Banking industry experts are unanimous: September 2025 represents a critical inflection point for Certificate of Deposit rates. With the Federal Reserve poised to slash rates, locking in today's yields could mean the difference between earning 4.50% APY and watching rates plummet to sub-4% levels.

"It's expected that CD rates will come down by the end of the year. The expected rate is about 25 basis points, with a possibility of 50 basis points by the end of the year. With rates expected to decline, delaying could mean missing out on better returns."— Krisstin Petersmarck, Founder at New Horizon Retirement Solutions

Smart CD Moves for September 2025

✅ Do This Now

- • Lock in 12-month CDs at 4.50%+ APY

- • Consider no-penalty CDs for flexibility

- • Build CD ladders with staggered terms

- • Shop online banks for highest rates

❌ Avoid These Mistakes

- • Don't lock up your entire emergency fund

- • Avoid long-term CDs without laddering

- • Don't choose CDs based on rates alone

- • Avoid banks with poor withdrawal terms

The no-penalty CD strategy deserves special attention. While these products typically offer rates 0.25-0.50% lower than traditional CDs, they provide crucial flexibility during uncertain economic times. With inflation pressures and potential market volatility ahead, the ability to withdraw funds without penalties could prove invaluable.

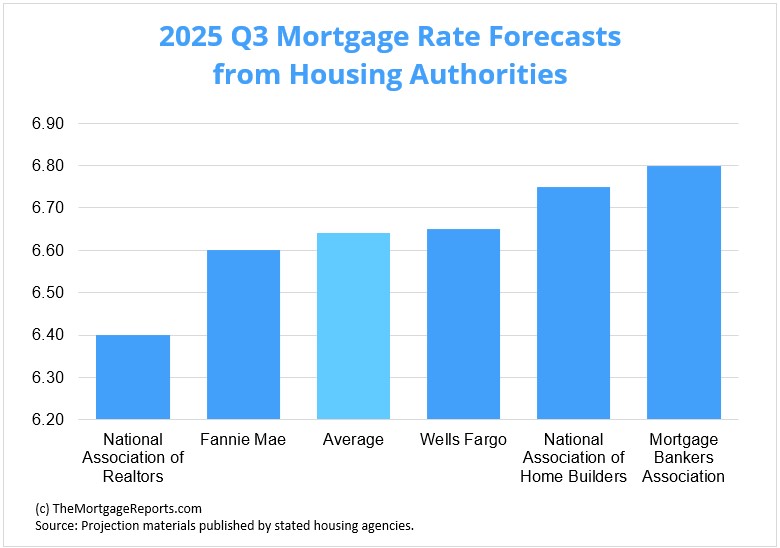

Mortgage Refinancing Rates Hit Sweet Spot for September Buyers

September 2025 presents a unique opportunity window for homebuyers and refinancing candidates. Current mortgage refinancing rates sit at 6.50% for 30-year fixed loans, with purchase rates slightly lower at 6.41%. Historical analysis suggests late September through early October traditionally offers the best home-buying conditions.

September Mortgage Rate Snapshot

Purchase Rates:

- 30-year fixed: 6.41%

- 15-year fixed: 5.55%

- 5/1 ARM: 6.50%

- VA 30-year: 5.89%

Refinance Rates:

- 30-year fixed: 6.50%

- 15-year fixed: 5.77%

- 5/1 ARM: 6.91%

- VA 30-year: 6.01%

Why September Is Prime Time for Home Purchases

Research from Realtor.com identifies the final week of September through early October as the optimal home-buying period. This timing advantage stems from reduced competition, motivated sellers, and historically favorable rate environments.

💡 Pro Tip: 15-Year vs 30-Year Mortgage Math

Consider this $400,000 mortgage comparison:

- 30-year at 6.41%: $2,505/month, $501,672 total interest

- 15-year at 5.55%: $3,279/month, $190,212 total interest

- Savings: $311,460 in interest over loan life

Credit Card Debt Reaches $1.21 Trillion: Emergency Relief Options

Americans are drowning in credit card debt, with national balances reaching a staggering $1.21 trillion in Q2 2025. With average credit card rates hovering near 22%, the math is brutal: carrying balances becomes exponentially expensive. However, several relief strategies can provide immediate breathing room.

Debt Relief Options Ranked by Effectiveness

1. Debt Consolidation Loans (Highest Success Rate)

Personal loan with low interest rates (typically 6-12%) can slash monthly payments by 40-60% compared to credit cards. Best for borrowers with credit scores above 650.

2. Balance Transfer Credit Cards

0% APR credit card offers provide 12-21 months of interest-free payments. Ideal for disciplined borrowers who can pay off balances during promotional periods.

3. Credit Card Forbearance

Temporary payment reduction or pause for borrowers experiencing documented financial hardship. Available through direct issuer contact and hardship verification.

4. Home Equity Line of Credit

Home equity line of credit rates (currently 7-9%) offer substantial savings over credit cards. Requires sufficient home equity and stable income.

⚠️ Warning: Credit Card Forbearance Requirements

Credit card forbearance isn't automatic. You must:

- Demonstrate legitimate financial hardship with documentation

- Maintain previous good payment history with the issuer

- Provide proof of ability to resume payments within 12 months

- Contact your issuer directly to request hardship consideration

Best Checking Accounts USA: September 2025 Winners

The checking account landscape has evolved dramatically, with best checking accounts USA now offering competitive yields and premium features that rival traditional savings products. For freelancers and small business owners, specialized accounts provide crucial benefits during uncertain economic times.

:max_bytes(150000):strip_icc()/how-to-open-a-high-yield-savings-account-4770631-final-c7f448b5c0bc48658a3c6a4c7afa0a3d.jpg)

Top Checking Account Categories

High-Yield Checking

- • APY up to 2.50%

- • No monthly fees

- • ATM fee reimbursement

- • Mobile deposit

Freelancer-Focused

- • Expense categorization

- • Tax document integration

- • Multiple savings goals

- • Invoicing tools

Student-Optimized

- • No minimum balance

- • Free overdraft protection

- • Credit building tools

- • Educational resources

Best bank accounts for freelancers have become essential tools for managing irregular income streams. Features like automatic expense categorization, integrated invoicing, and multiple savings buckets help independent contractors navigate the feast-or-famine cycle typical of freelance work.

💼 Freelancer Banking Strategy

Smart freelancers use a three-account system:

- Operating Account: Monthly expenses and immediate cash flow

- Tax Account: 25-30% of income set aside for quarterly payments

- Emergency Account: 6-month expense buffer in high-yield savings

Best Credit Cards for Students & Business Loan Strategies

September 2025 brings fresh opportunities for students and entrepreneurs to access favorable financing. Best credit cards for students now offer unprecedented rewards and credit-building features, while business loan for startups rates remain competitive despite broader economic uncertainty.

Student Credit Card Essentials

Top Student Features 2025:

- • Cashback rewards: 1-5% on student categories

- • Credit education: Free FICO score monitoring

- • Flexible terms: No annual fees or foreign transaction fees

- • Graduation bonuses: Credit limit increases after degree completion

Startup Financing Options

Business Loan Landscape:

- • SBA loans: 7-11% rates for qualified borrowers

- • Equipment financing: 8-15% for machinery/technology

- • Business lines of credit: 12-20% for working capital

- • Revenue-based financing: Alternative for service businesses

🎓 Student Credit Building Timeline

Follow this proven 24-month credit building strategy:

Months 1-6: Secured card with $200+ limit

Months 7-12: Student card upgrade with rewards

Months 13-18: Credit limit increases

Months 19-24: Premium card eligibility

Your September 2025 Banking Action Plan

The convergence of Federal Reserve rate cuts, record credit card debt, and seasonal mortgage opportunities creates a unique financial landscape requiring immediate action. Smart savers are locking in high yield savings account rates above 4.30% APY before inevitable declines, while strategic borrowers are leveraging debt consolidation loans and mortgage refinancing rates to reduce long-term costs.

September 2025 won't return again. The combination of competitive CD rates, favorable mortgage timing, and available credit relief programs creates a narrow window for financial optimization. Whether you're building emergency savings, consolidating debt, or preparing for homeownership, the strategies outlined above provide your roadmap for navigating this critical period.

Take Action Today

Don't let this opportunity slip away. Compare rates, contact lenders, and secure your financial future before September ends. Your future self will thank you for the rates you lock in today.

Share this guide with friends and family who could benefit from these time-sensitive strategies, and bookmark this page for updates as rates continue to evolve.

0 Comments