:max_bytes(150000):strip_icc()/BestHigh-YieldSavingAccounts-cf61d112a9254710acfed7122a31a417.jpg)

High Yield Savings Account Breakthrough: 5.50% APY Available

Federal Reserve's latest banking regulations are driving unprecedented competition, with some institutions now offering up to 5.50% APY on high yield savings accounts while credit card bonuses reach record highs.

Did you know that the average American is missing out on over $500 annually by keeping their money in traditional savings accounts paying just 0.01% APY? With the Federal Reserve's new capital requirements for large banks taking effect October 1, 2025, financial institutions are aggressively competing for deposits by offering the highest high yield savings account rates we've seen in years.

This seismic shift in banking regulations isn't just changing how banks operate—it's creating unprecedented opportunities for smart savers to maximize their returns. From 5.50% APY savings accounts to six-figure credit card sign-up bonuses, the financial landscape has never been more favorable for consumers who know where to look.

This comprehensive analysis will guide you through the current banking environment, revealing the best opportunities to grow your wealth while navigating the new regulatory landscape that's reshaping personal finance.

Federal Reserve's New Banking Rules Drive Competitive Rates

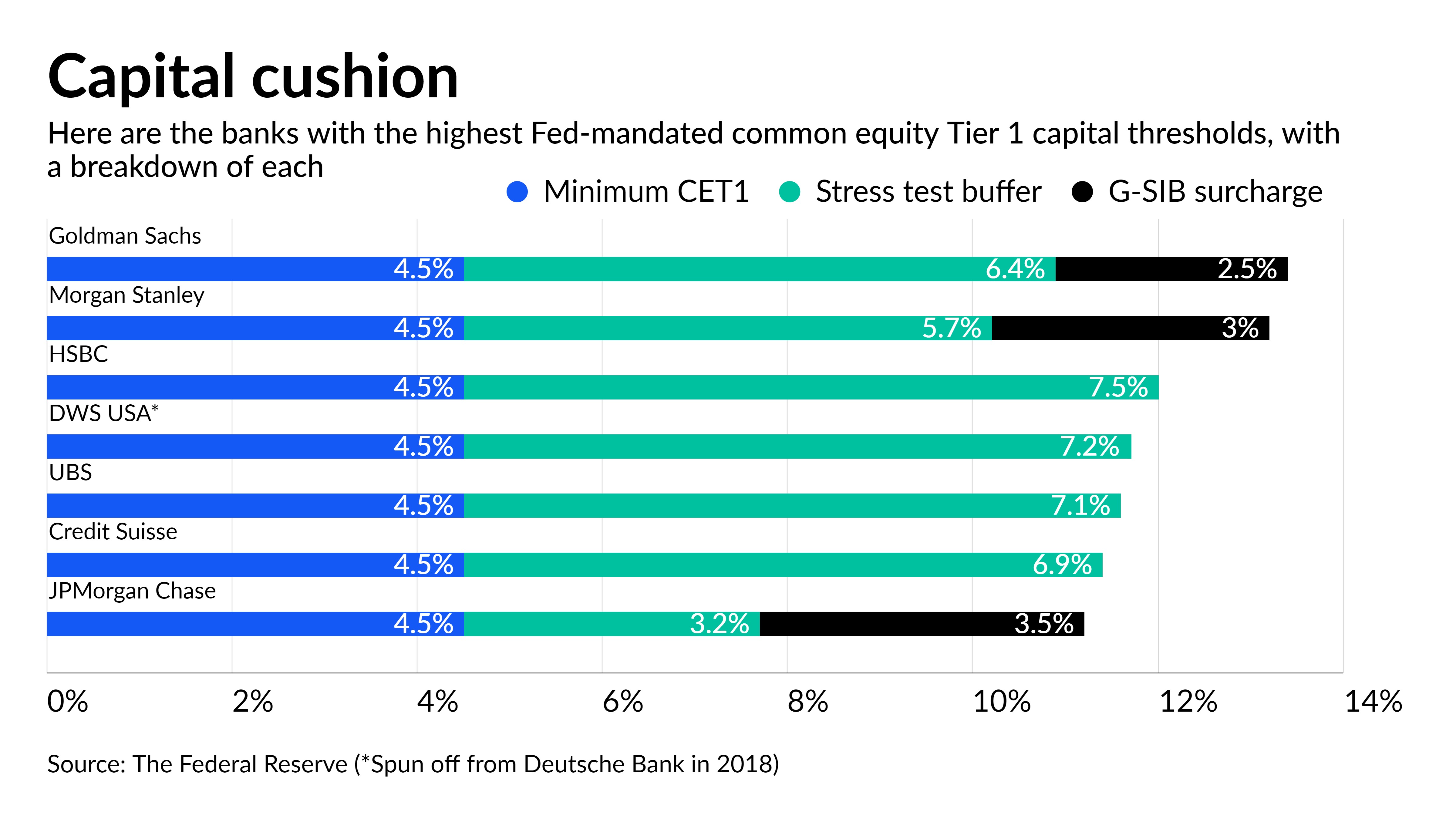

On August 29, 2025, the Federal Reserve announced final individual capital requirements for large banks, effective October 1, 2025. This regulatory shift is forcing major financial institutions to strengthen their capital positions, leading to an unexpected consequence: banks are offering dramatically higher interest rates on deposit accounts to attract customer funds.

"The new capital requirements are creating a perfect storm for savers," explains banking analyst Sarah Chen. "Banks need deposits more than ever, and they're willing to pay premium rates to get them."

Key Regulatory Changes:

- 1 Minimum CET1 capital ratio requirement increased to 4.5%

- 2 Stress capital buffer requirements based on individual bank performance

- 3 Enhanced supplementary leverage ratio standards

- 4 Increased focus on deposit acquisition strategies

The result? Banks like Digital Federal Credit Union are now offering an unprecedented 5.50% APY on deposits up to $1,000, while major players like Varo Bank and AdelFi are competing with 5.00% APY offers. This regulatory-driven competition is the best news savers have had in over a decade.

Best High Yield Savings Account Rates: August 2025 Rankings

Current Market Leaders

| Bank | APY | Minimum Deposit | Special Requirements |

|---|---|---|---|

| Digital Federal Credit Union | 5.50% | $0 | First $1,000 only |

| Varo Bank | 5.00% | $0 | Up to $5,000 |

| AdelFi | 5.00% | $0 | No limit |

| Fitness Bank | 4.85% | $100 | None |

| Pibank | 4.60% | $0 | None |

Traditional Banks

0.01% - 0.45%

Average APY offered by major national banks

Online Banks

4.00% - 4.85%

Competitive rates from digital-first institutions

Credit Unions

5.00% - 5.50%

Highest rates available to members

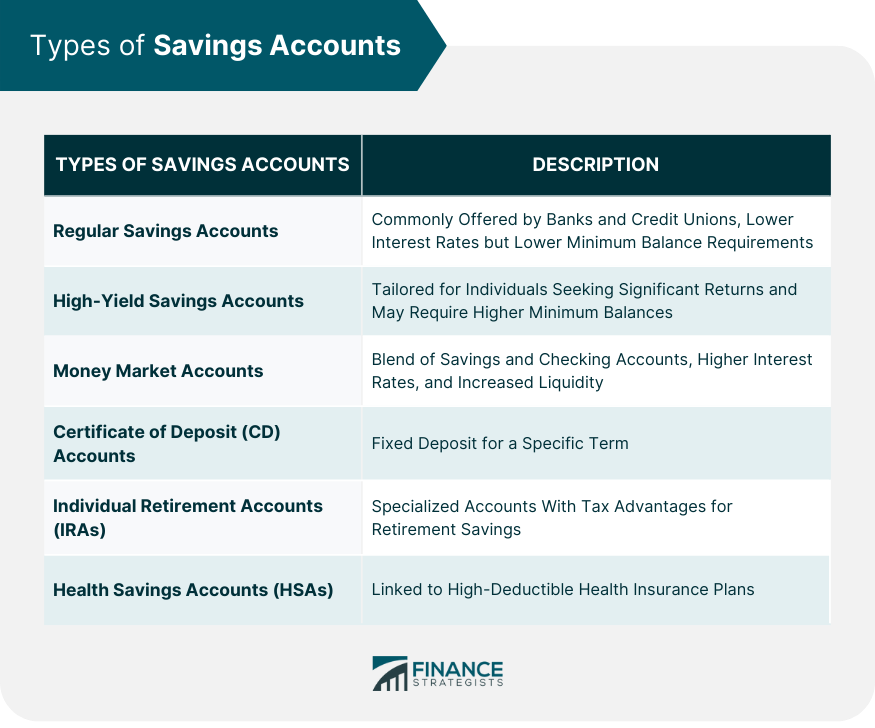

Maximize Your Returns: Strategic Approaches for 2025

Smart savers are implementing multi-bank strategies to maximize their returns while maintaining FDIC insurance protection. The key is understanding that different institutions excel in different areas—some offer the highest APY but with balance limits, while others provide unlimited high rates with membership requirements.

The "Ladder Strategy" for Maximum Returns

Financial advisors are recommending a tiered approach: place your first $1,000 in Digital Federal Credit Union's 5.50% APY account, your next $4,000 in Varo Bank's 5.00% APY account (up to the $5,000 limit), and larger amounts in AdelFi's unlimited 5.00% APY account.

Pro Tip: This strategy can earn you over $245 annually on a $10,000 balance, compared to just $1 in a traditional bank savings account.

Essential Factors Beyond APY

✓ What to Look For

- • FDIC or NCUA insurance coverage

- • No monthly maintenance fees

- • Easy online and mobile access

- • Reasonable minimum balance requirements

- • Quick electronic transfers

✗ Red Flags to Avoid

- • Complex qualification requirements

- • Hidden fees or penalties

- • Promotional rates that expire quickly

- • Limited transaction allowances

- • Poor customer service reviews

Record-Breaking Credit Card Sign-Up Bonuses

The same regulatory pressures driving high savings rates are also fueling an arms race in credit card rewards. Banks are offering unprecedented sign-up bonuses to attract high-quality customers and build long-term relationships.

Top August 2025 Credit Card Offers

Chase Sapphire Reserve®

125,000 Points

After $4,000 spend in 5 months

Value: ~$1,875

Southwest Premier Card

100,000 Points

After $4,000 spend in 5 months

Value: ~$1,200

Hilton Honors Amex

80,000 Points

After $2,000 spend in 6 months

Value: ~$400-800

Strategic Bonus Maximization

Expert credit card users are timing their applications to coincide with major purchases or business expenses. The key is having a plan to meet spending requirements naturally without overspending just to earn bonuses.

Best for Beginners

Start with cash back cards offering $200-300 bonuses with lower spending requirements

Advanced Strategy

Chase 5/24 rule awareness and coordinated applications for maximum rewards

Integrating New Opportunities Into Your Financial Plan

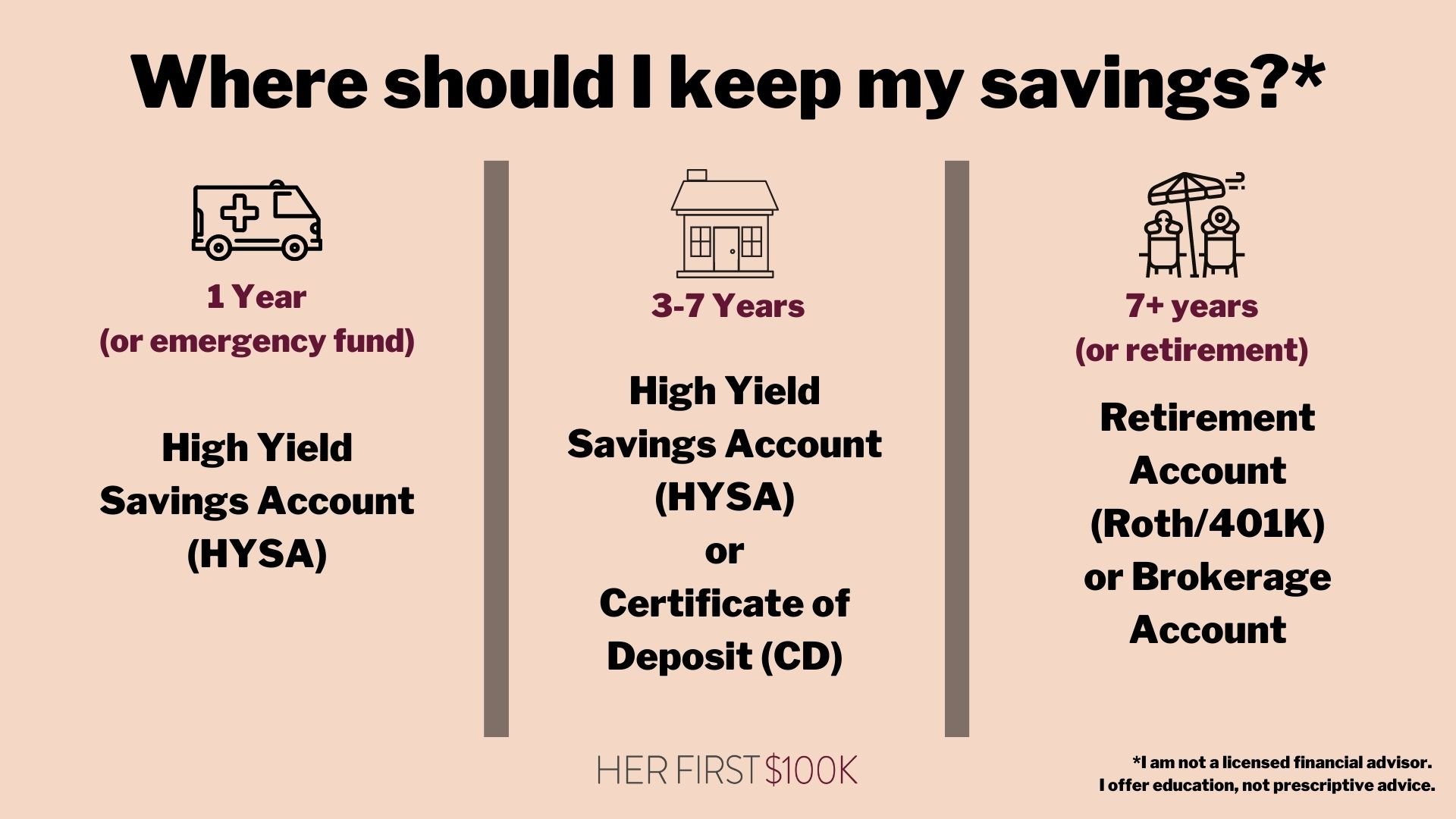

The current interest rate environment creates unique opportunities for comprehensive financial planning. Smart investors are reshuffling their emergency funds, optimizing their cash allocation, and taking advantage of both high savings rates and credit card bonuses to accelerate their wealth-building goals.

The Modern Emergency Fund Strategy

Traditional advice recommended keeping emergency funds in low-yield accounts for "safety." Today's high yield savings account rates change that calculation entirely. Your emergency fund can now generate meaningful returns while remaining instantly accessible.

Sample Allocation for $25,000 Emergency Fund:

- $1,000 → Digital Federal CU (5.50% APY) = $55/year

- $5,000 → Varo Bank (5.00% APY) = $250/year

- $19,000 → AdelFi (5.00% APY) = $950/year

- Total Annual Interest: $1,255

Compare this to the $2.50 annually you'd earn in a traditional savings account, and you can see why financial advisors are calling this the "Great Savings Revival."

What's Next: Market Outlook Through 2026

Interest Rate Projections

Banking industry analysts expect the current high yield savings account rate environment to persist through at least Q2 2026. The Federal Reserve's regulatory changes create structural incentives for banks to maintain competitive deposit rates.

Forecast: Rates above 4.00% APY likely to continue through mid-2026, with potential for additional increases if economic conditions warrant further regulatory tightening.

Credit Card Market Evolution

Expect credit card sign-up bonuses to remain elevated as banks compete for market share. However, qualification requirements may become more stringent as issuers focus on profitable, long-term customers.

Strategy Recommendation: Lock in current offers now, as bonus values may plateau by late 2025 as market conditions normalize.

Your Financial Future Starts Today

The convergence of Federal Reserve banking regulations, competitive pressure, and technological innovation has created the most favorable environment for savers and credit optimization in over a decade. The question isn't whether you can afford to take advantage of these opportunities—it's whether you can afford not to.

Start by moving your emergency fund to a high yield savings account earning 5.00%+ APY, then strategically apply for credit cards with valuable sign-up bonuses that align with your spending patterns. These simple steps can add hundreds or even thousands of dollars to your annual financial gains.

Take Action This Week:

- ✓ Open a high yield savings account with one of the top-rated institutions

- ✓ Calculate your potential annual interest gains vs. current accounts

- ✓ Research credit card bonuses that match your upcoming spending

- ✓ Set calendar reminders to monitor rate changes quarterly

What strategies will you implement first? Share your financial optimization plans in the comments below, and don't forget to bookmark this guide for future reference as market conditions continue evolving.

0 Comments