September 2025: Fed Rate Cuts Drive Mortgage Refinancing Boom

The Federal Reserve's anticipated September rate cut is reshaping the lending landscape, with mortgage refinancing rates dropping to 6-month lows and credit card APRs poised for relief. Are you positioned to capitalize on these shifts?

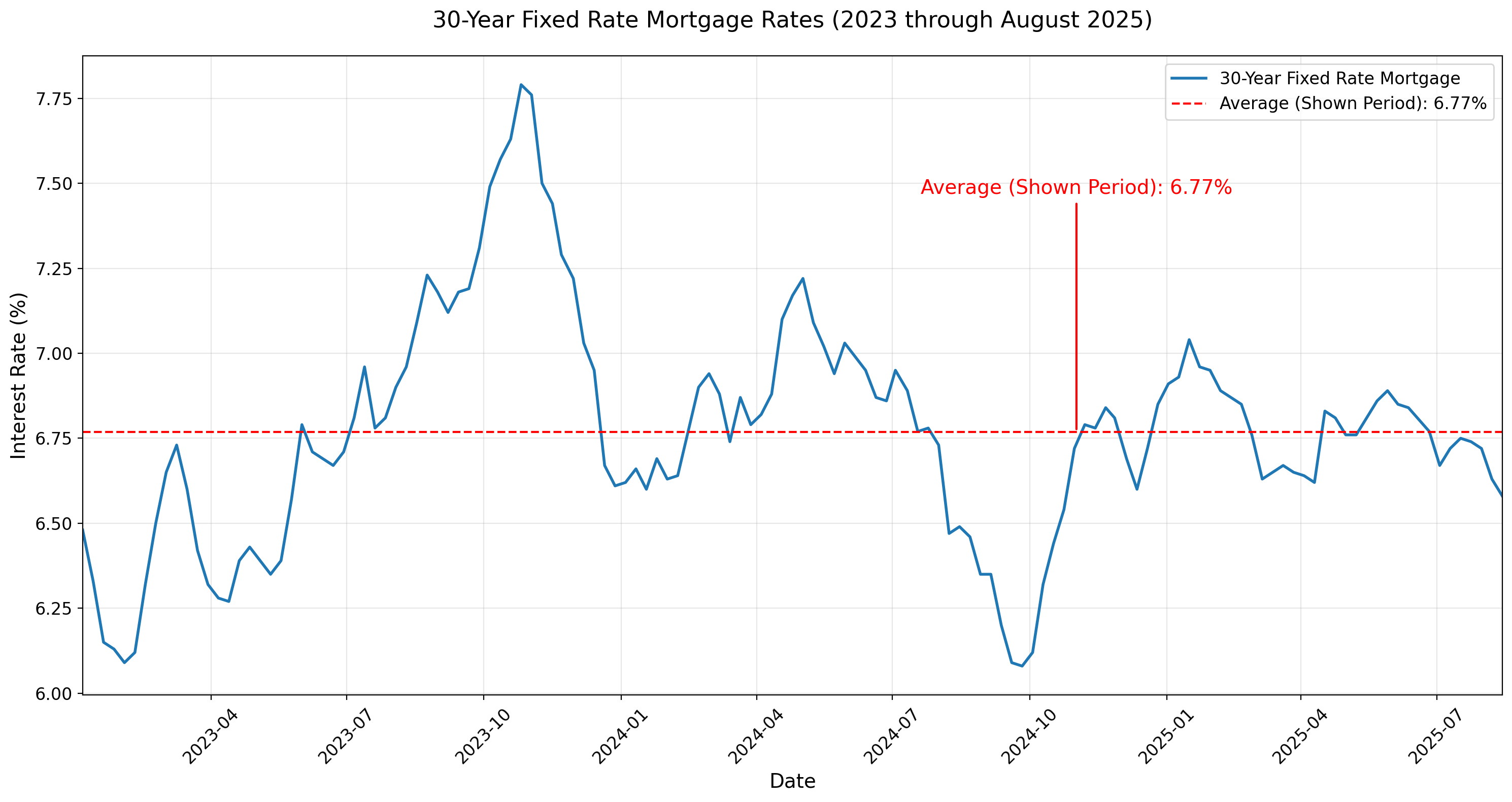

Did you know that mortgage rates have just hit their lowest point since March 2025, with the 30-year fixed rate dropping to 6.20%? This dramatic shift comes as financial markets prepare for the Federal Reserve's first interest rate cut in nearly a year, creating ripple effects across personal loans, credit card offerings, and refinancing opportunities.

September 2025 marks a pivotal moment for borrowers nationwide. With an 87% probability of a Fed rate cut this month, consumers are rushing to secure better terms on everything from mortgage refinancing rates to personal loans with low interest. The timing couldn't be more critical for your financial strategy.

From understanding how these rate changes impact your existing debt to identifying the best credit cards for students in this new environment, we'll explore every angle of this financial transformation and reveal actionable strategies to maximize your savings.

Mortgage Refinancing Rates Hit 6-Month Lows: Your Window of Opportunity

The mortgage market has experienced its most significant shift since early 2025, with the 30-year fixed mortgage rate plummeting to 6.20% according to Zillow's latest data. This 16 basis point drop represents the lowest point we've seen since October 2024, creating unprecedented opportunities for homeowners considering refinancing.

What makes this particularly compelling? Even a modest reduction from 6.5% to 6.2% on a $400,000 mortgage translates to approximately $67 in monthly savings—that's over $800 annually and more than $24,000 over the life of the loan.

🎯 Refinancing Strategy Alert

Current homeowners with rates above 6.5% should act quickly. Industry experts predict this rate environment may be temporary, with potential volatility expected as markets react to Federal Reserve decisions.

Real-World Impact Example:

Sarah, a Denver homeowner, refinanced her $350,000 mortgage from 7.1% to 6.2% this week, reducing her monthly payment by $198. Over 30 years, she'll save approximately $71,280 in interest payments—money that can now fund her high yield savings account or investment portfolio.

Federal Reserve Rate Cut: How It Transforms Your Debt Strategy

Federal Reserve Chair Jerome Powell's recent signals have markets pricing in an 87% probability of a September rate cut, with some economists predicting a 25-50 basis point reduction. This marks the first rate decrease since December 2024, and its implications extend far beyond mortgage markets.

The ripple effects will directly impact credit card APRs, personal loan rates, and auto financing costs. Since most consumer credit products are tied to the prime rate—which moves in lockstep with the federal funds rate—borrowers across America are positioned to benefit substantially.

Expected Rate Reductions

| Product Type | Current Avg. | Post-Cut Est. |

|---|---|---|

| Credit Cards | 23.99% | 23.49% |

| Personal Loans | 12.35% | 11.85% |

| Auto Loans | 7.18% | 6.68% |

| HELOC | 8.92% | 8.42% |

:max_bytes(150000):strip_icc()/ejOLS-federal-reserve-average-and-median-available-aprs4-a748861e380c4b1e86bad40ea44b5307.png)

"A 50 basis point Fed cut could save the average American household carrying $6,194 in credit card debt approximately $31 annually in interest charges—not massive, but meaningful relief in today's economy."

Best Credit Cards for Students and 0% APR Opportunities in the New Rate Environment

September 2025 has ushered in a competitive credit card landscape, with issuers offering aggressive promotions to attract new customers ahead of anticipated rate cuts. For students and young professionals, this timing creates exceptional opportunities to secure favorable terms.

The current environment favors balance transfer strategies and 0% APR credit card offers, as banks anticipate lower funding costs post-Fed cut. Smart consumers are leveraging these promotions for debt consolidation loans alternatives.

Student Cards

- • No annual fees trending

- • 1.5-2% cashback standard

- • Building credit features

- • Fraud protection enhanced

0% APR Offers

- • 15-21 months typical

- • $200-500 sign-up bonuses

- • Balance transfer options

- • No penalty APR promotions

Premium Features

- • Travel insurance included

- • Purchase protection standard

- • Mobile app enhancements

- • Real-time alerts

⚠️ Strategic Timing Consideration

Applications submitted before the Fed announcement may receive approval under current underwriting standards, potentially offering better terms than post-rate-cut applications as banks adjust their risk models.

Personal Loans with Low Interest and Home Equity Line of Credit Advantages

Personal Loan Market Shifts

The personal loan sector is experiencing significant rate compression, with average APRs expected to drop from 12.35% to approximately 11.85% following the Fed's September decision. For borrowers seeking personal loans with low interest, this represents meaningful savings opportunities.

Consider Marcus, a Portland resident consolidating $15,000 in credit card debt. A 50 basis point reduction in his personal loan rate saves him $75 annually—modest but significant when combined with the psychological benefit of fixed payments versus variable credit card rates.

- ✓Fixed-rate protection against future increases

- ✓Simplified payment structure

- ✓Lower overall interest costs vs. credit cards

HELOC Rate Environment

Home equity line of credit rates are particularly sensitive to Fed changes, with current averages around 8.92% expected to decline to 8.42%. For homeowners with substantial equity, this creates compelling opportunities for major expenses or investment strategies.

HELOC Strategy: With rates declining, homeowners are timing major renovations and investments to capitalize on lower borrowing costs while maintaining portfolio diversification.

High Yield Savings Account Rates and Best Checking Accounts USA: What to Expect

While borrowers celebrate declining loan rates, savers face the inevitable trade-off: high yield savings account rates will likely decrease following the Fed's September cut. Current rates averaging 4.25-5.00% may drop to 4.00-4.75%, though competition among banks could slow this decline.

The search for the best checking accounts USA becomes more nuanced in this environment. Banks are emphasizing service features, fee structures, and integrated financial tools rather than purely competing on interest rates.

Savings Strategy Adaptations

- 1 Lock in current rates with CDs before further declines

- 2 Diversify across multiple high-yield institutions

- 3 Consider money market accounts for rate stability

- 4 Evaluate investment alternatives for long-term goals

Checking Account Features to Prioritize

💡 Pro Tip: Online banks typically maintain higher savings rates longer than traditional banks during rate decline cycles. Consider splitting deposits between convenience (local bank) and yield optimization (online institution).

Your September 2025 Financial Action Plan: Maximize These Rate Changes

The convergence of declining mortgage rates, anticipated Fed cuts, and competitive lending markets creates a limited-time opportunity for strategic financial moves. How can you position yourself to benefit most from these shifts?

🎯 Immediate Actions (Next 30 Days)

- • Request refinancing quotes from 3+ lenders

- • Apply for 0% APR balance transfer cards

- • Lock current high-yield savings rates with CDs

- • Review existing variable-rate debt obligations

📋 Medium-term Strategy (60-90 Days)

- • Complete refinancing process if beneficial

- • Implement debt consolidation strategy

- • Reassess investment allocation post-rate changes

- • Optimize banking relationships for new environment

💰 Savings Optimization

- • Calculate refinancing break-even timeline

- • Diversify savings across rate-competitive institutions

- • Consider treasury securities for stable returns

- • Evaluate money market alternatives

🔄 Ongoing Monitoring

- • Track Fed meeting outcomes and market reactions

- • Monitor credit score for optimal loan terms

- • Review quarterly for additional opportunities

- • Stay informed on inflation and employment data

September 2025 Rate Environment Checklist

For Borrowers:

- □ Mortgage refinancing analysis completed

- □ Credit card balance transfer strategy implemented

- □ Personal loan rates compared across lenders

- □ HELOC applications submitted while rates decline

For Savers:

- □ High-yield accounts secured before rate drops

- □ CD ladder strategy evaluated for rate protection

- □ Banking relationships optimized for new environment

- □ Investment rebalancing considered post-rate changes

Seizing September's Financial Opportunities

September 2025 represents a pivotal moment in the personal finance landscape, with mortgage refinancing rates at 6-month lows and Federal Reserve rate cuts creating opportunities across lending markets. The convergence of declining borrowing costs and competitive promotional offers provides a narrow window for strategic financial optimization.

Whether you're pursuing mortgage refinancing rates for substantial monthly savings, securing personal loans with low interest for debt consolidation, or identifying the best credit cards for students in this favorable environment, timing remains crucial. These rate advantages won't persist indefinitely as markets adjust to the new Federal Reserve policy stance.

Ready to Optimize Your Financial Strategy?

Share your experience with rate changes in the comments below, or explore our comprehensive guides on maximizing savings in the evolving interest rate environment.

Article written by walletwhisperer

Published September 6, 2025 | Personal Finance & Banking News

0 Comments