:max_bytes(150000):strip_icc()/how-to-open-a-high-yield-savings-account-4770631-final-c7f448b5c0bc48658a3c6a4c7afa0a3d.jpg)

High Yield Savings Account Rates Drop: Smart Banking Moves

Did you know that high yield savings account rates have dropped from their 2024 peaks, yet still offer returns 10 times higher than traditional savings accounts? With the Federal Reserve's recent policy adjustments, September 2025 presents both challenges and opportunities for savvy savers and borrowers.

Today's banking landscape requires strategic thinking as mortgage refinancing rates hover around 6.44%, debt consolidation loans remain competitive, and students navigate evolving credit card offers. Whether you're maximizing your emergency fund returns or considering a major financial move, understanding these shifts is crucial for your financial success.

We'll explore current rates across savings accounts, mortgages, and loans, plus reveal actionable strategies to optimize your banking relationships in this changing environment.

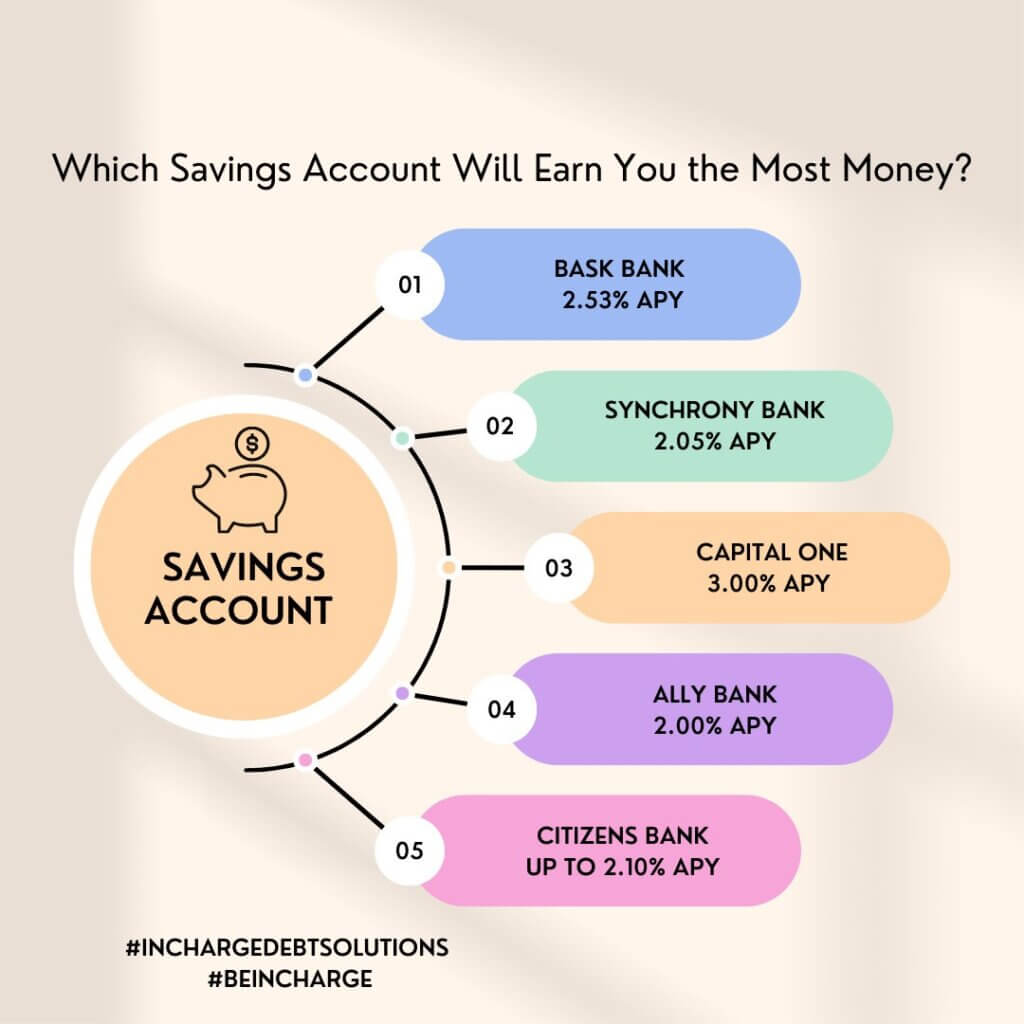

Current High Yield Savings Account Landscape

The high yield savings account market has experienced significant shifts in September 2025. While rates have declined from their 2024 highs, the best accounts still offer impressive returns compared to traditional banking options. EverBank and Western Alliance currently lead the pack with 4.30% APY, representing a substantial opportunity for savers.

High yield savings accounts offer significantly better returns than traditional savings options

Top High Yield Savings Rates

- EverBank 4.30% APY

- Western Alliance 4.30% APY

- Varo Bank 5.00% APY*

- AdelFi 5.00% APY*

*Conditions may apply

💡 Expert Insight

"Even with recent rate declines, today's high yield savings account options still outperform traditional savings by 1000% or more. The key is acting quickly, as rates continue their downward trajectory following Fed policy changes."

For Americans building emergency funds or saving for short-term goals, these rates represent a golden opportunity. Consider Sarah, a freelance graphic designer from Austin, who moved her $15,000 emergency fund from a traditional bank offering 0.05% APY to a high yield savings account at 4.30% APY—earning an additional $640 annually while maintaining full liquidity.

Mortgage Refinancing Rates Show Mixed Signals

Mortgage refinancing rates present a complex picture in September 2025. The current average for a 30-year fixed refinance sits at 6.44%, while 15-year options average 6.20%. These rates remain elevated compared to the pandemic-era lows but show signs of stabilization following recent Federal Reserve decisions.

| Loan Type | Current Rate | Previous Week | Change |

|---|---|---|---|

| 30-Year Fixed Refi | 6.44% | 6.59% | -0.15% |

| 15-Year Fixed Refi | 6.20% | 6.35% | -0.15% |

| 5/1 ARM | 5.57% | 5.73% | -0.16% |

| Jumbo 30-Year | 7.08% | 7.15% | -0.07% |

When Refinancing Makes Sense

- ✓ Current rate is 1%+ higher than available rates

- ✓ Planning to stay in home 3+ years

- ✓ Need to access home equity

- ✓ Want to switch from ARM to fixed-rate

:max_bytes(150000):strip_icc()/2-22Line-f1b1b2765f7243b896e202d28545054c.png)

Mortgage refinancing rates show recent downward movement

Take the example of Michael and Jennifer from Denver, who purchased their home in 2023 with a 7.2% mortgage rate. With current mortgage refinancing rates at 6.44%, they could save approximately $180 monthly on their $400,000 loan—justifying the refinancing costs within 18 months. However, homeowners with rates below 5% from earlier years should carefully calculate whether refinancing makes financial sense.

Debt Consolidation Loans Remain Attractive Option

Debt consolidation loans continue offering relief for Americans struggling with high-interest credit card debt. With average credit card APRs exceeding 20%, a personal loan with low interest rates between 6-12% can provide substantial savings and simplified payment management.

:max_bytes(150000):strip_icc()/debtconsolidation.asp-final-18e80676e0af4379a7962bfc4a0874de.png)

Debt consolidation can significantly reduce monthly payments and interest costs

Debt Consolidation Benefits

- 💰 Lower interest rates (6-12% vs 20%+ credit cards)

- 📅 Single monthly payment

- ⏰ Fixed repayment timeline

- 📈 Potential credit score improvement

📊 Real-World Example

Before Consolidation: Lisa from Phoenix had $25,000 across 4 credit cards at an average 22% APR, paying $650 monthly with minimum payments.

After Consolidation: She secured a personal loan with low interest at 8.5% APR, reducing her monthly payment to $485 and saving over $8,000 in interest over 5 years.

Top Debt Consolidation Lenders September 2025

SoFi

Best Overall

5.99% - 24.99% APR

LightStream

Best for Large Loans

7.49% - 25.49% APR

Discover

Best for Low APRs

6.99% - 24.99% APR

The current environment favors borrowers seeking debt consolidation loans, as lenders compete aggressively for qualified applicants. However, success requires discipline—consolidating debt without addressing spending habits often leads to accumulating new debt alongside the consolidation loan.

Best Credit Cards for Students Navigate Rate Changes

The best credit cards for students market remains robust despite broader economic shifts. Student cards continue offering valuable rewards, 0% APR credit card offers, and credit-building opportunities essential for establishing financial independence during college years.

Top Student Credit Cards September 2025

Capital One Savor Student

Best for Dining & Entertainment

- • 3% cash back on dining, entertainment, streaming

- • 1% on all other purchases

- • No annual fee

Discover it® Student Cash Back

Best Overall Value

- • 5% rotating categories (up to $1,500/quarter)

- • 1% on all other purchases

- • Cashback Match for first year

Building credit early with student cards creates long-term financial advantages

🎓 Student Success Story

Emma, a sophomore at UCLA, strategically uses her Discover it® Student card for textbooks during 5% book category quarters and dining with her Capital One Savor Student card. She's earned over $400 in rewards while building a 720+ credit score—positioning herself for premium cards and better loan rates post-graduation.

Smart Student Banking Strategy

Credit Building Tips

- • Keep utilization below 10%

- • Pay full balance monthly

- • Set up automatic payments

- • Monitor credit score regularly

Maximize Rewards

- • Use category bonuses strategically

- • Combine with high yield savings account

- • Track spending with apps

- • Redeem rewards regularly

Students should pair their best credit cards for students with a high yield savings account to maximize their financial foundation. This combination provides both credit building and competitive returns on emergency funds—essential elements for post-graduation financial success.

Smart Banking Strategies for the Current Market

Navigating September 2025's banking landscape requires strategic thinking and quick action. With rates in flux and opportunities shifting, successful savers and borrowers must adapt their approaches to maximize benefits while minimizing risks.

🏦 Optimize Savings

- • Lock in current high yield savings account rates

- • Consider CD laddering for rate protection

- • Diversify across multiple institutions

- • Monitor rate changes weekly

🏠 Mortgage Moves

- • Calculate refinancing break-even points

- • Shop multiple lenders for mortgage refinancing rates

- • Consider ARM options for short-term ownership

- • Explore cash-out refinancing opportunities

💳 Credit Optimization

- • Consolidate high-interest debt now

- • Apply for 0% APR credit card offers

- • Maximize category bonuses before changes

- • Build credit with responsible usage

Action Plan for Next 30 Days

Week 1-2: Assessment

- • Review current account rates and fees

- • Calculate potential savings from switches

- • Check credit scores and reports

- • List all debts and interest rates

Week 3-4: Implementation

- • Open new high yield savings account

- • Apply for debt consolidation if beneficial

- • Submit refinancing applications

- • Set up automatic transfers and payments

Remember that the best checking accounts USA institutions offer often complement high-yield savings with features like ATM fee reimbursements, mobile check deposits, and integrated financial planning tools. Consider your complete banking relationship, not just individual product rates, when making decisions.

Take Action on Today's Banking Opportunities

September 2025's banking landscape offers clear winners for proactive consumers. High yield savings account rates above 4% APY won't last forever, and current mortgage refinancing rates show signs of stabilization that could benefit qualified borrowers.

Whether you're maximizing savings returns, consolidating debt, or building credit as a student, the key is acting decisively while opportunities remain available. The financial institutions are competing for your business—make sure you're positioned to benefit.

Ready to optimize your banking strategy?

Share this guide with friends who could benefit, and bookmark our site for weekly rate updates and financial insights.

Article written by walletwhisperer

0 Comments